- GasTurbineHub Newsletter

- Posts

- Gas Turbines in a Fragmenting World: From Commodity Hardware to Strategic Infrastructure

Gas Turbines in a Fragmenting World: From Commodity Hardware to Strategic Infrastructure

In a world that fears disruption more than emissions, flexible turbine capacity is becoming strategic again

In partnership with EthosEnergy

As every first Saturday of each month, welcome to this month’s edition of the GasTurbineHub Newsletter!

In today’s newsletter:

📈 Geopolitics Reshapes Turbine Demand – What it means for key stakeholders.

🏭 Gas Turbine New Installations – Latest updates on projects and deployments.

⚙️ Gas Turbine Technology Developments – Innovations driving efficiency and performance.

🔥 Low Carbon Gas Turbines – Advancements in low-carbon-powered solutions.

📅 2026 Events Calendar – Upcoming industry events and opportunities to connect.

📣 Together With EthosEnergy

EthosEnergy delivers tailored gas turbine solutions that transform uncertainty into performance. The company's services enhance reliability, extend asset life, streamline operations, and reduce lead times through OEM quality expertise, advanced repairs, and customized full scope maintenance support.

As an OEM for the Westinghouse and FiatAvio mature fleets, EthosEnergy provides full OEM level support. In addition, EthosEnergy offers comprehensive independent services across GE Vernova® Frame B, E, and F Class turbines, MHI® M and MW fleets, Siemens Energy® SGT600, Siemens Westinghouse® W501D5–5A and W251B12, and ABB Alstom™ GT11.

Its portfolio covers rotor manufacturing and life extension, field and outage services, parts supply and repairs, combustion optimization, and flexible long term service agreements - maximizing uptime, controlling costs, and maintaining efficiency.

Visit www.ethosenergy.com.

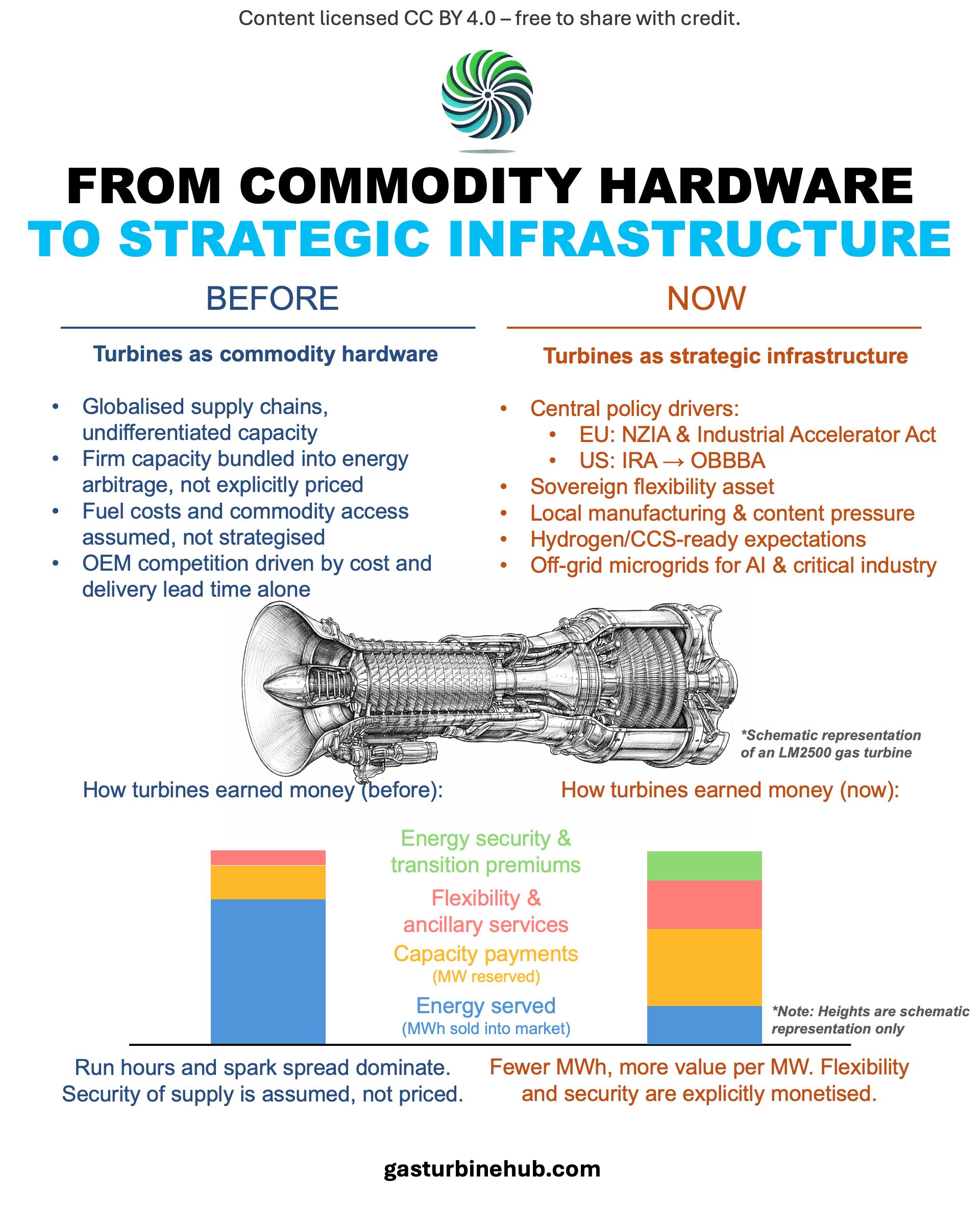

Gas turbines are quietly being reclassified: no longer “just another generation option,” but sovereign infrastructure sitting at the intersection of energy security, industrial policy, and a new wave of electrification. The irony is that this rediscovery comes precisely as the long‑term policy narrative tries to move beyond gas.

In a world this unstable, understanding that wider system context is no longer optional for gas turbine decisions, it is the difference between merely following the market and actually seeing where it is going.

Let’s jump right in!

From Globalisation to Energy Bloc Politics

The old model assumed that fuels, components, and capital would flow freely across borders, and that the cheapest marginal kilowatt-hour would win. That world ended when energy became a frontline instrument of statecraft: Russia’s war in Ukraine, US–China strategic competition, and weaponised pipeline and LNG flows made resilience and controllability the new currencies of power.

The EU’s Net‑Zero Industry Act1 explicitly aims to secure at least 15% of global manufacturing capacity in key net‑zero technologies by 2040, while forcing oil and gas producers to underwrite at least 50 million tonnes per year of CO₂ storage capacity by 2030 in depleted fields. Complementing this, the Commission’s new Industrial Accelerator Act2 proposal pushes “Made in EU” and low‑carbon content requirements into public procurement and support schemes, creates industrial manufacturing acceleration areas, and introduces tighter screening and localisation conditions for large foreign investments in strategic clean‑tech and energy‑intensive sectors.

In parallel, the US Inflation Reduction Act (IRA)3 initially rewired incentives toward renewables, storage, nuclear and clean hydrogen via extended production and investment tax credits, while also boosting CCS economics through an enhanced 45Q regime. Under the Trump administration, the 2025 “One Big Beautiful Bill Act”4 has not repealed the IRA, but it has accelerated the phase‑out and narrowed the scope of several clean‑energy tax credits, turning what was designed as a multi‑decade support architecture into a more compressed, politically fragile window.

Asia has moved in its own direction: China is building a “green fortress” around domestic clean‑energy manufacturing and diversified fossil imports, while Asia–Pacific more broadly is on track to dominate gas turbine deployment on the back of rapid industrialisation and energy security‑driven combined‑cycle build‑out.

Macro Shifts Reshaping the System

De‑globalisation and re‑shoring are reshaping where turbines, components and fuels come from. Trade tensions and sanctions are fragmenting supply chains, prompting OEMs and states to favour regional manufacturing footprints and trusted corridors for fuels like LNG. For a technology whose large frames historically depended on deeply internationalised casting, forging and control‑system supply networks, this is not a theoretical risk; it is already visible in bid conditions and qualification rules.

Energy security has quietly overtaken pure decarbonisation as the organising principle of many systems. LNG markets have swung from around 9 to 16 USD per MMBtu across recent winters, while Europe now sources over 60% of its imported gas as LNG, reinforcing the premium on efficiency and ramping capability in gas fleets. Each percentage point of combined‑cycle efficiency now translates into millions per year in fuel savings, effectively turning modern turbines into financial hedging instruments against fuel volatility.

Electrification is adding a new, non‑linear demand driver: AI and data‑centre load. Global data‑centre consumption is already estimated in the 650–800 TWh range and could triple by 20305, with US grid planners facing 7–10 GW per year of new high‑quality load requests and connection queues of 5–8 years in key markets. Hyperscalers are responding by building private microgrids, where gas turbines offer the only dispatchable, scalable solution on a 12–24‑month horizon; outages now carry contractual penalties in the millions per hour and load can grow 50–70% annually at some sites, pushing reliability to the core of the business model.

All of this unfolds against a backdrop of renewed industrial policy and critical‑materials stress. Support for clean energy in the IRA, NZIA and Asian industrial strategies accelerates renewables and storage, but also creates congestion, permitting delays, and competition for transformers, inverters, and grid equipment, reinforcing short‑to‑medium‑term dependence on existing gas turbine fleets and new firm capacity.

Why Gas Turbines Sit in the Crosshairs

Gas turbines occupy the uneasy centre of this landscape. On one axis, they are still the fastest‑to‑market source of dispatchable capacity at grid scale, especially in markets facing AI‑driven electrification and retiring coal. On another axis, they are the technology that policymakers most want to phase down over the long run in favour of “clean energy” options.

System dynamics reflect this dual role. As renewables expand, combined-cycle plants lose generation share, while open-cycle turbines retain critical value as low-utilisation peaking assets. In other words, megawatt-hours may move away from gas, but megawatts of turbine capacity remain indispensable. The problem is that this does not automatically translate into investable business models: a system can depend on gas turbines for security of supply while still failing to create the revenue certainty needed to modernise existing fleets or, in some cases, to justify building new ones.

At the same time, policy frameworks are keeping gas in play through CCS and hydrogen pathways. OEMs are marketing hydrogen‑ready turbines and low‑NOₓ combustors, while industrial users and policymakers increasingly demand credible pathways to 20–50% hydrogen co‑firing over the life of an asset. However, uncertainties around costs, infrastructure, and technical constraints of large-scale hydrogen firing remain unresolved, clouding the long-term operating profiles and asset values of current projects.

The result is a peculiar configuration: structurally higher short‑term reliance on gas turbines for flexibility, security and new digital loads, paired with policy‑driven long‑term uncertainty about their allowed running hours, fuel mix, and cost of capital.

Implications for Industry Actors

OEMs. In the next 0–3 years, OEMs will benefit from a clear seller’s market, using backlog pressure to reprice risk, prioritise strategic markets, and regionalise supply chains. Over the longer term (3–15 years), competitiveness will hinge on offering fuel and policy optionality, hydrogen-ready systems, CCS-compatible designs, and digital optimisation. The shift is from hardware suppliers to sovereign infrastructure partners; those that fail to adapt risk being constrained by policy and declining utilisation.

Utilities and IPPs. In the short term, firm capacity is being treated as an insurance product, driving earlier investment decisions, tighter turbine procurement, and focus on flexibility (ramping, part-load efficiency, dual-fuel capability). Over time, portfolios will shift toward low-utilisation, high-value flexibility assets supported by capacity and ancillary markets. Designing plants today with CCS and hydrogen pathways will be critical to maintaining long-term viability and political acceptance.

Oil & Gas companies. In the near term, these players remain central to gas and LNG supply but are increasingly expected to deliver integrated, lower-carbon power solutions. This includes combining turbines with CCS and industrial clusters. Over 3–15 years, competitive advantage will come from bundling molecules with infrastructure, gas, storage, turbines, and carbon capture, into resilience platforms. Pure upstream strategies risk losing relevance as capital shifts toward integrated energy solutions.

Industrial users and data centres. In the short term, large energy users are deploying turbine-based microgrids to secure reliable power amid grid constraints, balancing speed, efficiency, and exposure to fuel and carbon costs. Longer term, they face strategic decisions: extend gas-based systems with hydrogen/CCS pathways or transition to alternative firm technologies like SMRs or long-duration storage. These choices will define future cost structures, risk profiles, and negotiating power.

Risks: Fragmented Supply, Incoherent Policy, Unclear End‑States

The risk landscape is as important as the opportunity set. Fragmented supply chains and export controls can delay turbine projects, raise EPC costs, and complicate cross‑border service models, especially for fleets relying on specialised components and centralised repair hubs. Policy unpredictability, swinging between aggressive support for gas as a security tool and sudden regulatory crackdowns on emissions, creates real stranded‑asset risk, particularly for unabated baseload projects commissioned late in this decade.

Technology uncertainty is equally material. Hydrogen‑ready badges are cheap to print but expensive to deliver at scale; material embrittlement, NOₓ control, and fuel‑supply constraints could limit practical co‑firing well below headline numbers in many markets, undermining transition plans built around high‑H₂ operation. Capital allocation becomes a high‑stakes puzzle: overcommit to gas turbines and you may own underutilised hardware in a deeply decarbonised grid; undercommit, and you risk being the system that discovers too late it lacks firm capacity for its own transition.

Opportunity in the Fragmentation

The same forces increasing risk are also opening one of the most attractive windows for gas turbines in decades. Market fragmentation is not just a constraint, it is enabling the rise of regional manufacturing and service hubs, where selected OEMs and suppliers can position themselves as quasi-national champions, embedded in sovereign energy strategies and partially shielded from global competition.

At the same time, energy security concerns, AI-driven demand growth, and coal retirements are driving strong order books, premium pricing for high-efficiency and fast-ramping units, and growing demand for reserved capacity and fast-deployment solutions. As grids become more volatile and saturated with renewables, the value of flexibility is rising, prompting policy shifts toward capacity and ancillary mechanisms that increasingly reward dispatchable, reliable turbine fleets.

Policy support is also playing a dual role. While targeting the phase-out of unabated fossil generation, it is channeling significant investment into CCS, hydrogen, and industrial clusters, areas where gas turbines remain central in transition configurations. The key distinction is strategic: actors treating this as a temporary subsidy cycle will fall short, while those recognising it as the foundation of a lower-carbon, gas-anchored system will shape the role of turbines in the coming decades.

Despite an apparently chaotic landscape, such as geopolitical fragmentation, conflicting policies, and competing capital priorities, the underlying direction is clearer from a turbine perspective. A world defined by electrification, energy security concerns, and low tolerance for outages structurally favours flexible, fuel-agnostic technologies. The critical question is not whether this window exists, but how long it remains open, and which players move decisively enough to capture it.

Looking ahead: Those who insist on a binary view, gas as either “over” or “untouchable”, will misprice both risk and opportunity; those who treat turbines as sovereign infrastructure embedded in a changing political economy will find that this period of disorder may, in hindsight, have been the most advantageous entry point the industry will see for a long time.

References: 1. Regulation (EU) 2024/1735 of the European Parliament and of the Council of 13 June 2024. 2. European Commission, COM(2026) 100 final, Industrial Accelerator Act, 4 March 2026. 3. Inflation Reduction Act of 2022, Public Law 117‑169, enacted 16 August 2022 as H.R. 5376. 4. One Big Beautiful Bill Act (OBBBA), enacted in the 119th Congress as H.R. 1, and published as Public Law 119‑21 on 4 July 2025. 5. IEA (2025), Energy and AI.

Join the conversation: Sign up for our newsletter to stay updated on developments in gas turbine technology and the energy sector.

Intelligence and Insights Reports - Stay ahead

|  |

Gas Turbine New Installations

Malakoff Secures Two Additional Mitsubishi Gas Turbines To Strengthen National Energy Generation Capacity

Malaysian independent power producer Malakoff announced a second Reservation Agreement with Mitsubishi Power for two M701JAC heavy-duty gas turbines (and generators) for a new 1,400 MW combined-cycle plant in northern Malaysia. This brings the total reserved Mitsubishi units for Malakoff to four, underscoring rising CCGT demand.

Source: Malakoff (2 March, 2026)Doosan Enerbility Wins First Steam Turbine Order for North American Combined Cycle Power Plant

Doosan Enerbility announced that it had signed a contract with a U.S. client to supply the company with seven units of its 380MW gas turbine. Starting in May 2029, Doosan is to sequentially deliver gas turbines and generators, one of each per month, to the data center being built by the client. With this recently won contract, Doosan Enerbility now has a total of 12 gas turbines to deliver in the United States.

Source: Doosan Enerbility (6 March, 2026)VinEnergo Hai Phong LNG Power Plant to Use GE Vernova Gas Turbines and Generators

GE Vernova has been selected by VinEnergo as the core equipment supplier for the Hai Phong LNG power plant. Under the agreement, GE Vernova shall supply two 9HA.02 gas turbines and two H78 generators in phase I, with a capacity of 1600 MW, to ensure the plant can begin operations by the end of 2030.

Source: Financial Times (11 March, 2026)Doosan Enerbility Wins First Steam Turbine Order for North American Combined Cycle Power Plant

Doosan secured a contract to supply two 370 MW‑class steam turbines and generators to a U.S. customer for data‑center power, building on earlier gas‑turbine orders and positioning Doosan as a combined‑cycle solutions provider in the North American AI data‑center market.

Source: Doosan Enerbility (18 March, 2026)JERA’s 500 MW hybrid CCGT project advances Hawaii’s LNG and gas-power strategy

JERA has submitted a proposal for a roughly 500 MW hybrid combined‑cycle and simple‑cycle gas plant fueled by imported LNG, aiming to replace oil‑fired units and provide fast‑ramping CCGT capacity to stabilize Hawaii’s grid.

Source: JERA (18 March, 2026)China's first 550 MW F-class gas turbine unit commences operation

China's first 550-megawatt F-class gas turbine unit started to generate electricity on Saturday after a 168-hour full-load trial run, marking a new breakthrough in the application of large-capacity, high-efficiency clean energy equipment in the country.

Source: CGTN (22 March, 2026)Fermi America(TM) Secures $165 Million Equipment Financing Facility to Accelerate Delivery of Six SGT-800 Gas Turbines for 2028 Delivery at Project Matador

Project Matador combines clean natural gas, advanced nuclear, solar, and battery storage into a single, integrated HyperGrid™. Anchored by Siemens Energy SGT-800 gas turbines as the near-term foundation, the campus is designed to ultimately generate 17GW of firm, low-carbon, on-demand power.

Source: Fermi (27 March, 2026)

Gas Turbine Technology and Market Developments

Musk’s xAI wins permit for datacenter’s makeshift power plant despite backlash

Elon Musk’s artificial intelligence company xAI won approval on Tuesday to run 41 methane gas turbines at its “Colossus 2” datacenter in northern Mississippi. That’s nearly double the amount it has been operating.

Source: The Guardian (10 March, 2026)Baker Hughes, Petrobras Sign Strategic Service Agreement for Critical Turbomachinery Equipment

Long-term agreement covers maintenance, repairs and advisory services for up to 64 aeroderivative gas turbines critical to Brazil’s offshore and refinery operations. Work to be delivered from the Baker Hughes Service Center in Petrópolis, Rio de Janeiro, with plans for further expansion of capacity and capability, strengthening Brazil’s energy supply chain.

Source: Baker Hughes (18 March, 2026)Hanwha Power Systems and PSM unite as Hanwha Power, a global compressor and gas turbine business

Hanwha Impact's subsidiaries, Hanwha Power Systems and PSM (Power Systems Mfg., LLC), a U.S.-based gas turbine service company, announced that they will integrate their brands and change the company name to “Hanwha Power.” The unified brand will seek to proactively address the rapidly evolving demands of the global power generation market.

Source: Hanwha (25 March, 2026)Ansaldo Energia closes 2025 with an improvement in its main economic and financial indicators and return into profitability after several years

The year ended with a positive net result of €20 million. Orders reached €2.3 billion, up 24% compared to the previous year, while revenues amounted to €1.2 billion, with an increase of 10%. Adjusted EBITDA rose to €140 million and EBIT returned to positive territory at €31 million.

Source: Ansaldo Energia (01 April, 2026)

Gas Turbine Decarbonisation News

Kawasaki & Kobe launch next-generation liquefied-hydrogen fuel supply system for gas turbines

At Kobe Hydrogen Energy Center, a system combining liquefied‑hydrogen pumps and an Intermediate Fluid Vaporizer began supplying hydrogen to a demonstration gas turbine, reducing compression energy and enabling efficient hydrogen fueling of future large‑scale turbines.

Source: Kawasaki (10 March, 2026)IHI and GE Vernova achieve milestone with 100% ammonia combustion in large scale test

Full‑scale combustor components operated at F‑class pressures, temperatures and flows on 100% ammonia, with emissions aligned to a roadmap for commercial 100% ammonia‑fired F‑class turbines by around 2030.

Source: GE Vernova (18 March, 2026)

Gas Turbine Related Events Happening in March

This month’s events are just a snapshot.

Explore more than 30 upcoming gas turbine conferences, exhibitions and user group meetings on GasTurbineHub.

Western Turbine Users (WTUI) Conference 2026

Date: April 7–10, 2026

Location: Long Beach, California (In-person)

Organizer: WTUI

Website: https://gasturbinehub.com/event/western-turbine-users-wtui-conference-2026/

V94.2 (SGT5-2000E AE94.2) Users Conference 2026

Date: April 20–23, 2026

Location: Helsinki, Finland (In-person)

Organizer: GTUsers

Website: https://gasturbinehub.com/event/v94-2-sgt5-2000e-ae94-2-users-conference-2026/